Institutional Insights: Citadel Global Markets Insights Oct´25

Global Market Insights October Takeaways ✅

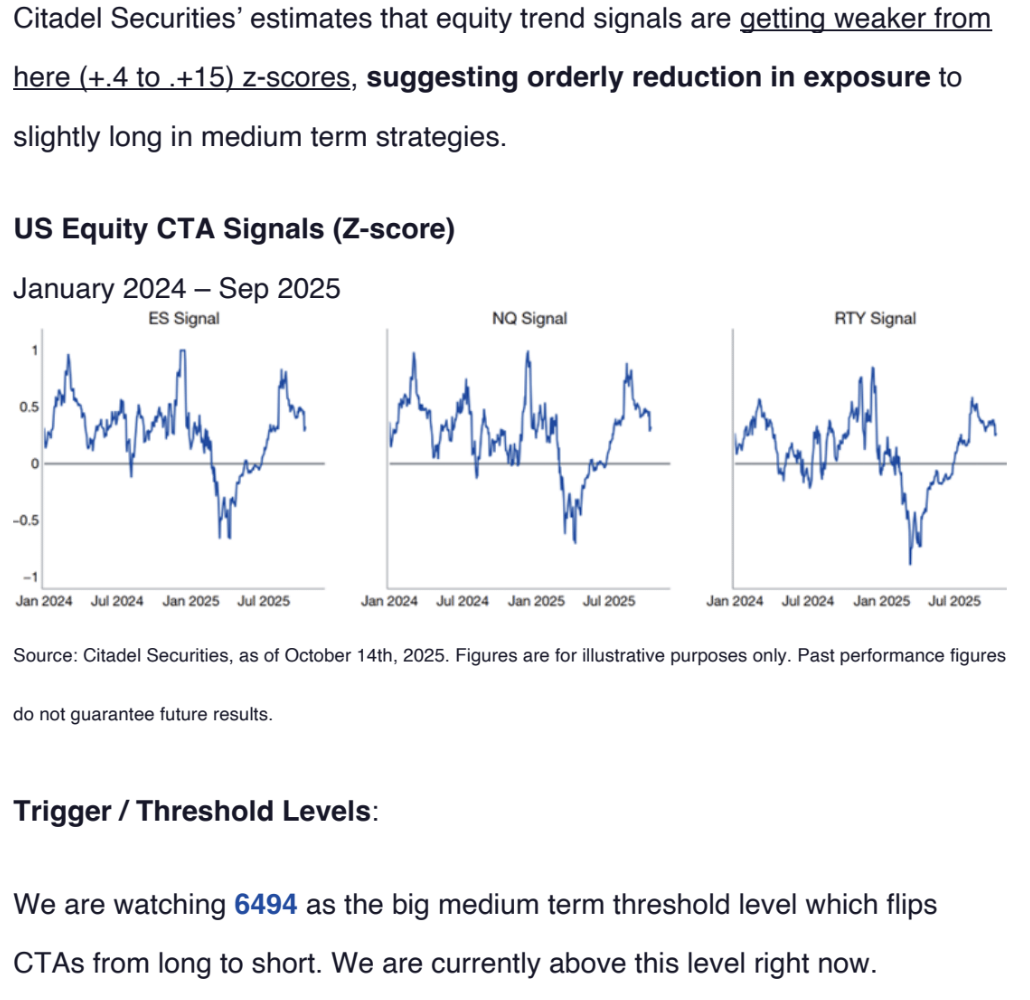

🚀 Theme: Structural Bull; Tactical October Fragility Persists

- Structural Bull: Retail demand, corporate buybacks, passive inflows, and AI-driven themes continue to provide strong market support.

- Tactical Risk: October remains fragile; consider hedging crowded positions ahead of earnings and potential headline risks.

- Forward View: A year-end FOMO rally appears likely—view second-half October dips as strategic buying opportunities.

- Rotation Watch: Expect potential catch-up flows in 493 stocks, Emerging Markets (EM), Value, and International sectors.

- Anti-Momentum Trend (Nov-Dec): Post mutual fund year-end, lagging stocks are likely to outperform. Near-term headline risks may continue to drive market volatility, but the primary trend of the equity market remains positive. Strengthening corporate fundamentals are expected to support the next upward move as we enter November, a historically strong month for equities.

Stay attentive to positioning and exposure over the next two weeks, with equity market activity running above average levels. Non-fundamental, systematic equity supply and daily rebalancing could potentially cause short-term market dislocations, so close monitoring is advised.

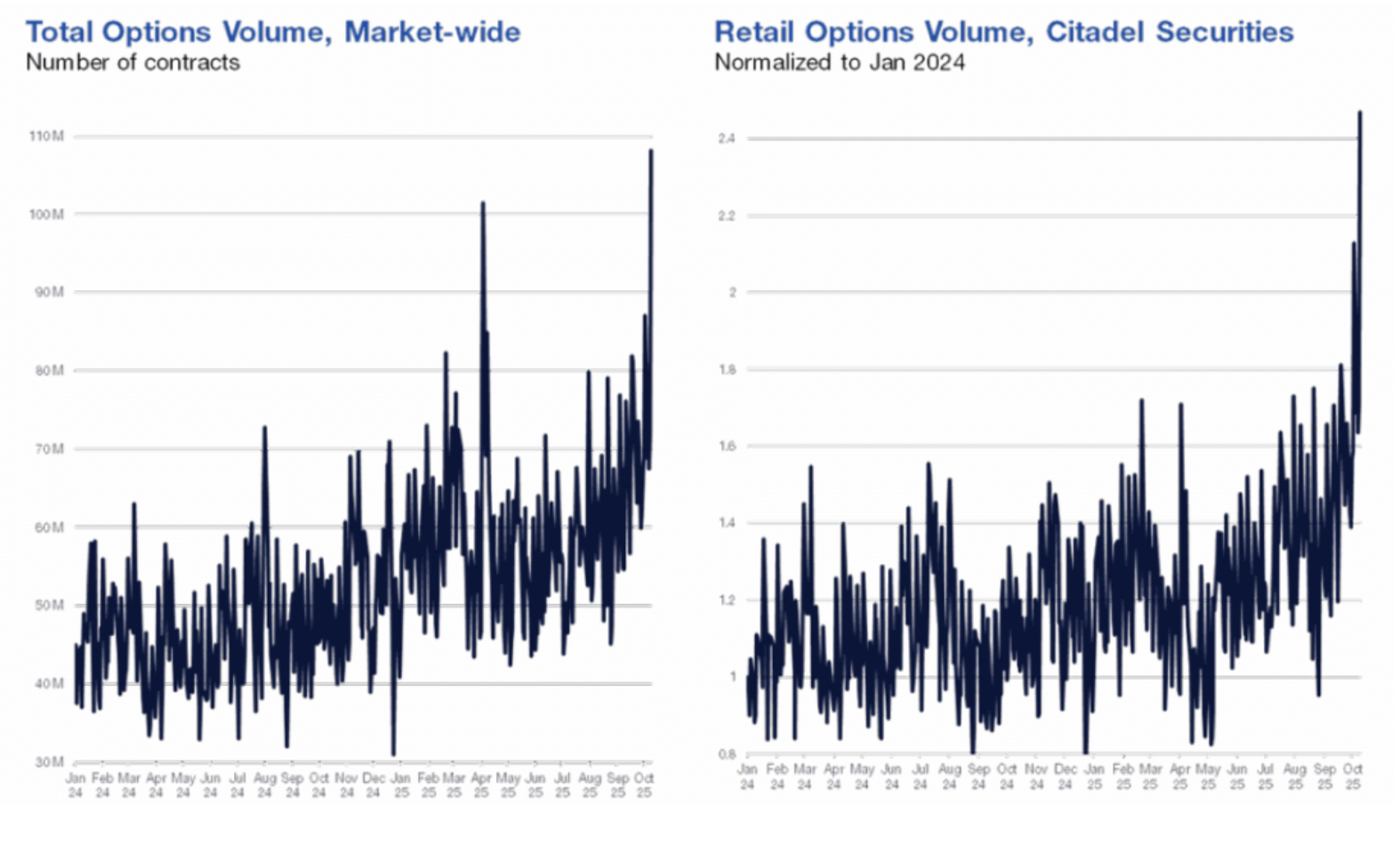

Options Activity: Retail’s Bullish Sentiment Persists

- On Friday, October 10th, the market witnessed the largest options trading day in history, with over 108 million contracts traded. This was only the second time daily volume surpassed 100 million, the first being April 4 (“Liberation Day”), when the SPX dropped by 6% (Source: Citadel Securities’ Allie Becher).

- Market-wide options flow was 73% higher than the 3-month average, with exceptionally high retail activity observed. Retail traders’ bullish conviction remains remarkable, marking the 24th consecutive week of a “better-to-buy” options skew, tying the record for the longest bullish streak on the platform.

- Friday’s surge exemplified the “buy-the-dip” mentality. Retail flows were skewed 11% better to buy, as indicated by the Call/Put Direction ratio (compared to a 4% average over the past three months). This marked the largest single-day call buying event ever recorded on the platform.

‘Retail Is Still Buying the Dip’ – Comparing Friday’s Selloff to April

Contrary to widespread market speculation, retail investors did not reduce their exposure during Friday’s selloff. At Citadel Securities, we analyzed retail trading flows and observed the following:

- Strong Net Buying Activity: Retail investors showed net buying activity across cash, options, and ETFs, marking the second-highest gross activity day ever recorded (only behind January 27, 2021).

- ETF Focus on Large-Cap Indices: ETF flows registered a +1.7 z-score to buy, with a focus on large-cap indices like the S&P 500 and Nasdaq. Notably, 36 cents of every dollar invested in SPY went to the “Magnificent 7” stocks.

- Bullish Options Sentiment: Retail investors were 11% net buyers of call options, contrasting sharply with institutional investors, who were 23% net buyers of put options, highlighting a bullish retail sentiment versus institutional hedging behavior.

In comparison to April’s de-grossing event—when retail activity showed a -6 z-score for selling on April 7—Friday’s data underscores the resilience of retail investors in buying the dip, even amidst mixed flows from China, which were not heavily skewed toward selling.

Additionally, last week, Citadel Securities hosted its annual Future of Global Markets Conference, bringing together over 350 clients and thought leaders for two days of discussions on key structural forces shaping today’s markets.

Key insights from the retail panel include:

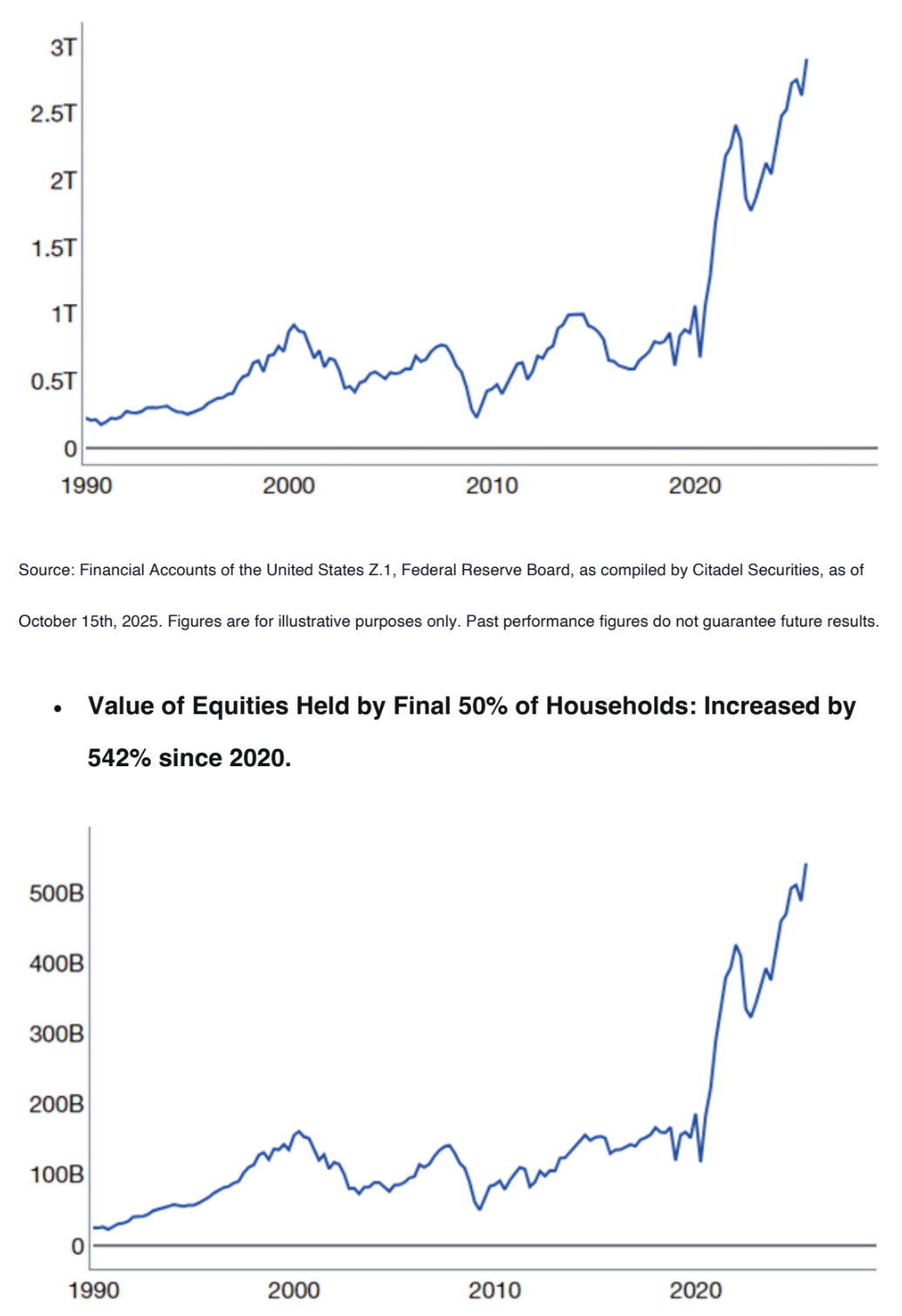

- Equity Ownership by Younger Investors: The value of equities held by households under 40 years old has surged by 300% since 2020, reflecting a significant generational shift in market participation.

Client Activity (Citadel Securities)

Key Points:

Retail investors are focusing on smaller "storybook" stocks, while institutional investors are hedging against macro risks but still maintain a benchmark-long position ahead of the Mutual Fund year-end (October 31).

- Retail Equities: Net buyers for 23 of the last 26 weeks, including 7 consecutive weeks.

- Retail Options: Achieved a record net buying streak of 24 weeks.

- Retail ETFs: Purchased ETFs on 206 out of 208 trading days.

- Institutions: Engaged in hedging macro longs for 8 of the last 9 weeks.

II. S&P Q3 Earnings Outlook

Earnings season begins this week, starting with major banks.

- Q2 Summary: Consensus expected growth of 5% YoY; actual growth was 11%, with 81% surpassing estimates.

- Q3 Outlook: Slightly elevated expectation with a consensus of 7.5% YoY.

- SPX three-month implied correlation remains low, indicating a market favorable to stock selection.

- Options indicate an earnings-day movement of approximately 4.7%, the highest since 2022; technology stocks lead with an expected move of about 5.9%.

- There is a significant disparity between index and single stock skew.

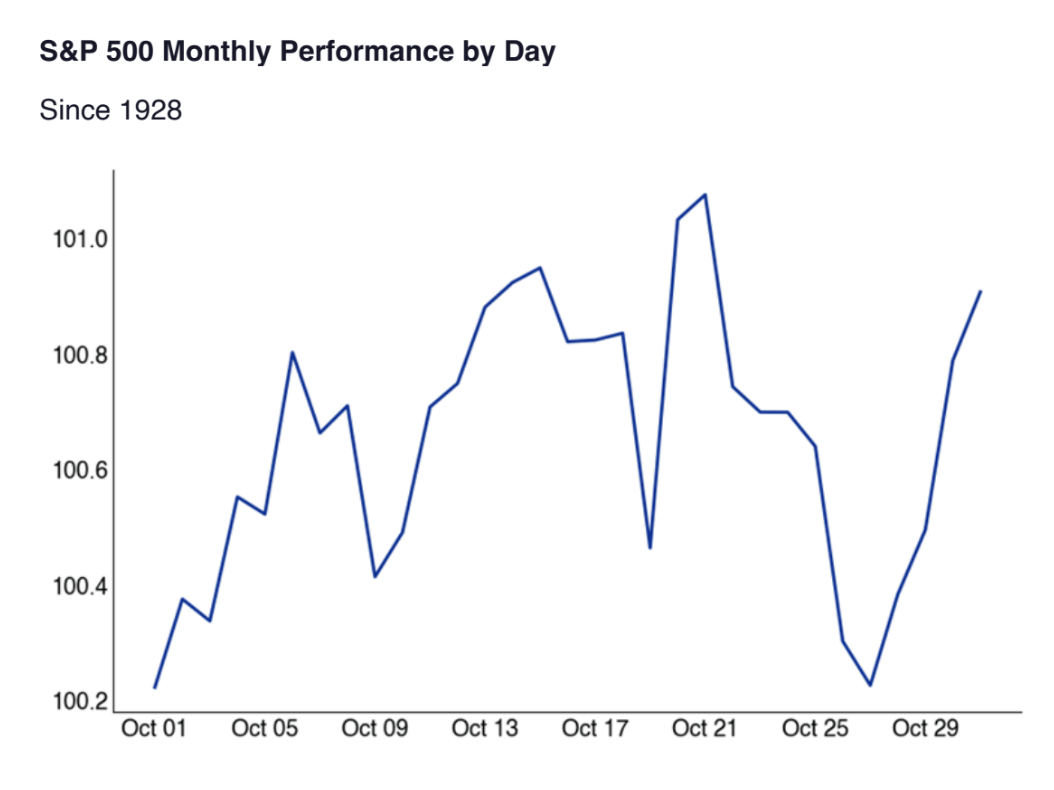

Year-End Seasonality | Starting October 26

Insights from a Century of Data:

• October is consistently one of the most volatile months for stock markets.

• Generally, October 26th serves as the low point for Q4 in the S&P 500, while October 27th marks the Q4 low for the Nasdaq 100. Enjoy Halloween!

• Dips in late October often lead to significant rallies as the year comes to a close.

• Years that perform well heading into Q4 usually see even stronger gains toward year-end.

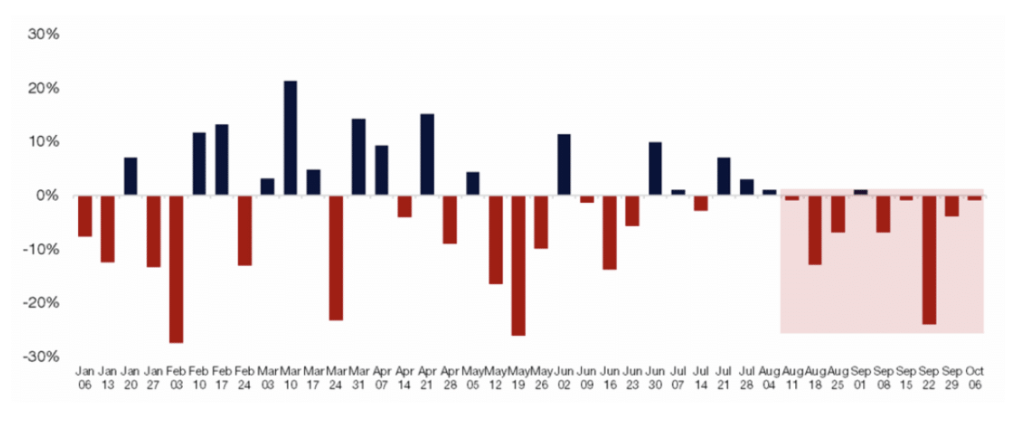

Institutional Options clients at Citadel Securities have been exhibiting hedging behavior, being bearish for 8 out of the past 9 weeks. The implied volatility has decreased, making hedges appealing while maintaining long positions. There is an increasing "fear of material underperformance" (FOMU) relative to benchmark indices, which has encouraged the persistence of long positions, especially amid ongoing trends in large-cap equities. Our macro clientele is seeking to counteract the recent surge in the lower-quality segments of the market. The analysis of Call/Put Direction Ratios by week indicates bearish flows from January to October 2025.

Peak Corporate Blackout Window

- Today marks the PEAK blackout window. Typically, blackout periods begin about two weeks before quarter-end and conclude a day or two after Q3 earnings. August experienced strong buyback activity during the open window.

- According to EventVestor, U.S. buyback authorizations have exceeded $1.297 trillion for the Russell 3000, marking the fastest pace on record. This figure could potentially reach $1.5 trillion by year-end. Assuming a 90% execution rate, this translates to $1.35 trillion in actual executions, setting a new record. S&P 500 companies alone have recorded $1.064 trillion in authorizations year-to-date. Monitor this trend closely following Q3 earnings reports.

- Buyback dynamics: Approximately $1.35 trillion in VWAP executions spread over 251 trading days implies an estimated $5.3 billion in daily buyback demand.

- Historically, November and December are the strongest months for U.S. corporate buyback executions. It is anticipated that companies will utilize their authorizations by the end of 2025. The current blackout window concludes on November 1st.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 71% and 74% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!