Institutional Insights: Deutsche Bank Investor Flows & Positioning 20/10/25

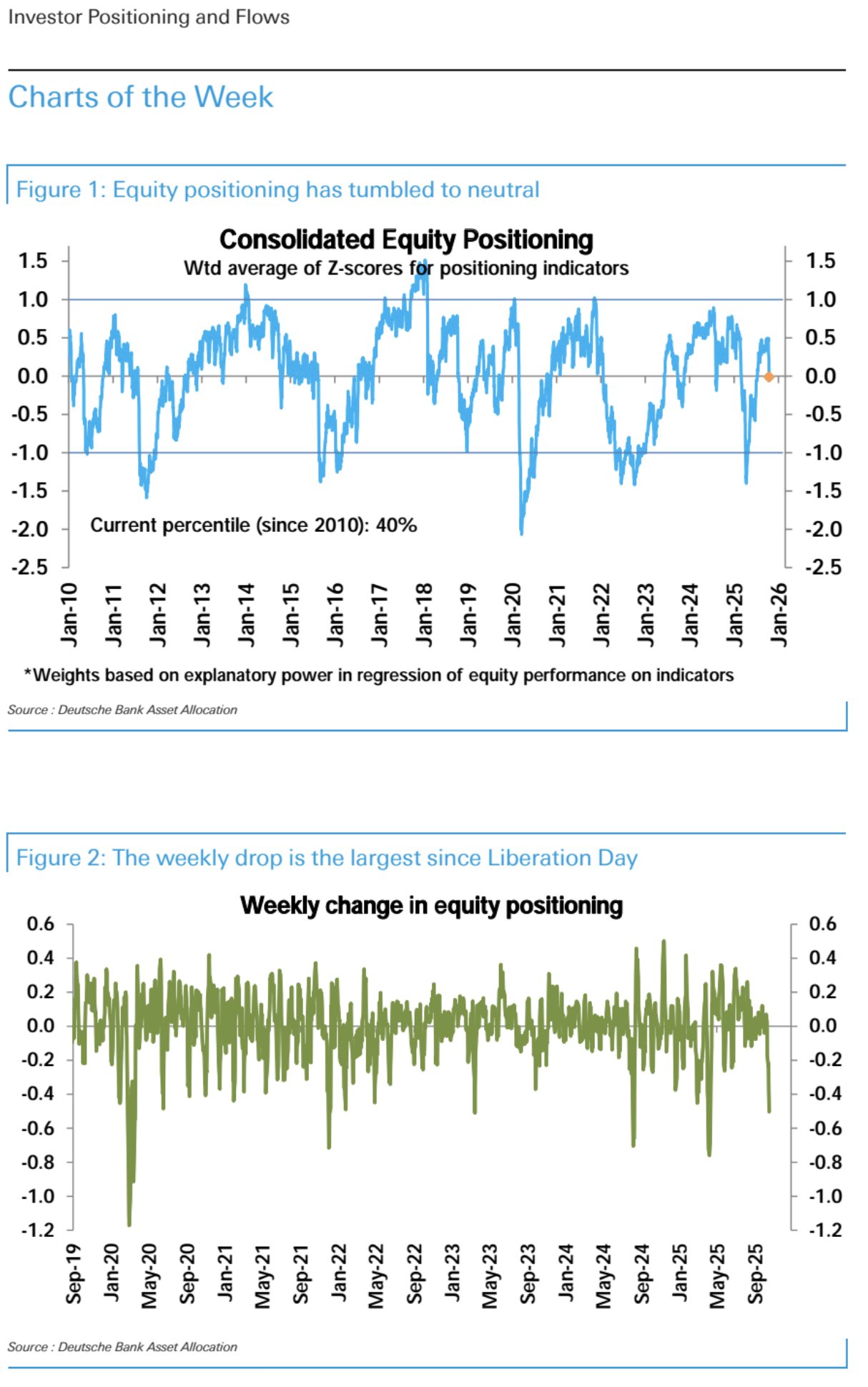

Equity positioning has taken a significant hit since last Friday, shifting from moderately overweight to neutral (-0.01 standard deviations, 40th percentile). This marks the largest weekly reduction since Liberation Day.

Systematic strategies have also scaled back their positions, dropping from elevated levels to a moderately overweight stance (0.55 standard deviations, 73rd percentile). If volatility remains high, further unwinding of exposures may be necessary.

Meanwhile, discretionary investors, who have been laser-focused on potential risks for months, have shifted from a neutral position to being notably underweight (-0.46 standard deviations, 20th percentile). They seem to be bracing for negative earnings growth in Q3, despite signs that growth is on track to reach low double digits—consistent with our projections. In fact, Financials, which have been leading the reporting season so far, are poised to deliver earnings growth exceeding 20% year-over-year. This outpaces both the bottom-up analyst consensus of 13% and even our own forecast of 16.4%.

Momentum-chasing trades, which had been rampant in certain areas despite broader caution among discretionary investors, are finally retreating. While these trades only experienced a minor hiccup last Friday and even surged earlier this week, they have sharply pulled back over the past two days.

Equity fund inflows remain robust, though they are highly selective. Over the past five weeks, equity funds have attracted a staggering $162 billion, with $28 billion flowing in just this week. However, these inflows are concentrated in specific regions and sectors. The U.S. and China have been the primary beneficiaries geographically, while sectors such as Technology, Financials, Industrials, and increasingly Materials—driven by heightened interest in metals and rare earths—are seeing the most activity. On the other hand, bond fund inflows have slowed significantly to just $5.8 billion this week, the weakest level since April. High-yield bonds, emerging market debt, and bank loan funds all saw substantial outflows.

Interestingly, recent market volatility has been concentrated during U.S. trading hours, while overnight trading has seen steady gains. This mirrors a pattern observed last year and contrasts sharply with the brief period of turbulence around Liberation Day.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 71% and 74% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!