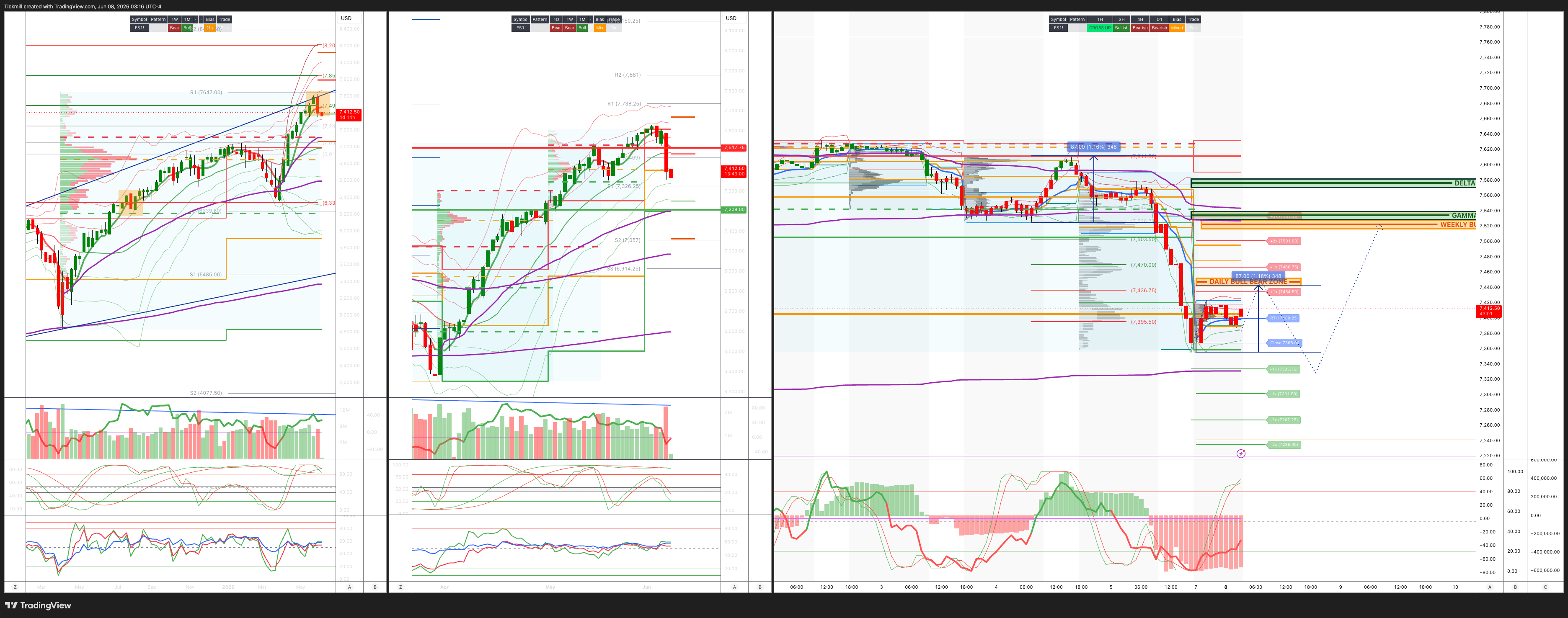

S&P500 Daily Action Areas & Price Targets 8/6/26

S&P500 Daily Action Areas & Price Targets 8/6/26

***QUOTING ES1! FOR CASH US500 EQUIVALENT LEVELS, SUBTRACT POINT DIFFERENCE***

WEEKLY BULL BEAR ZONE 7515/25

WEEKLY RANGE RES 7517 SUP 7208

June MOPEX Straddle: 274pt range implies a OPEX to OPEX range of [7134, 7683]

June QOPEX Straddle is 546.4pt giving us a range of [5960,7052]

JHEQX Q2 Collar 6189/6290 - 6865/6955

DEC2025 OPEX to DEC2026 OPEX is 945 points giving us a range of [5889,7779]

SPX PUT/CALL RATIO 1.09 (The numbers reflect options traded during the current session. A put-call ratio below 0.7 is generally considered bullish, and a put-call ratio above 1.0 is generally considered bearish)

DAILY VWAP BEARISH 7519

WEEKLY VWAP BEARISH 7477

MONTHLY VWAP BULLISH 7036

DAILY STRUCTURE - OTFD 7553

WEEKLY STRUCTURE - BALANCE 7354/7632

MONTHLY STRUCTURE - OTFH - 7199

Balance: This refers to a market condition where prices move within a defined range, reflecting uncertainty as participants await further market-generated information. Our approach to balance includes favouring fade trades at the range extremes (highs/lows) while preparing for potential breakout scenarios if the balance shifts.

One-Time Framing Higher (OTFH): This represents a market trend where each successive bar forms a higher low, signalling a strong and consistent upward movement.

One-Time Framing Lower (OTFL): This describes a market trend where each successive bar forms a lower high, indicating a pronounced and steady downward movement.

DAILY BULL BEAR ZONE 7445/55

GAMMA FLIP 7530

DELTA FLIP 7570

DAILY RANGE RES 7666 SUP 7333

2 SIGMA RES 7501 SUP 7267

VIX BULL BEAR ZONE 19

TRADES & TARGETS

SHORT ON REJECT/RECLAIM DAILY BULL BEAR ZONE TARGET DAILY RANGE SUP

***ADDITIONAL SETUPS & TARGETS HIGHLIGHTED ON THE CHARTS***

(I FADE TESTS OF 2 SIGMA LEVELS ESPECIALLY INTO THE FINAL HOUR OF THE NY CASH SESSION AS 90% OF THE TIME WHEN TESTED THE MARKET WILL CLOSE ABOVE OR BELOW THESE LEVELS)

GOLDMAN SACHS TRADING DESK VIEW - ‘Colour On The Week’

Hot NFP Triggers Risk-Off, but the Selloff Was Narrower Than the Index Suggested

US equities went risk-off into the weekend, with the Nasdaq 100 down 477bps and the S&P 500 down 265bps after a much hotter-than-expected payrolls print, follow-through weakness after AVGO earnings, and negative AI narrative pressure from Anthropic recursive learning headlines. The move was violent in price terms, but notably, activity levels did not pick up materially, and derivatives desks saw limited panic demand for hedges. That suggests the selloff was driven more by positioning, factor unwind, and crowded-theme liquidation than by broad institutional capitulation.

The headline index damage was severe, particularly in Tech. The NDX closed the week down 430bps, erasing the prior two weeks of gains, and Friday’s one-day move was the index’s worst since April 2025. The SOX fell 970bps on the day and finished the week down 420bps. The technical backdrop was demanding: earlier in the week, SOX had been trading roughly 75% above its 200-day moving average, the most extended level since the 1999/2000 era. That made the group highly vulnerable to any catalyst that challenged the AI/semi narrative or pushed rates higher.

The NFP report was the macro trigger. Nonfarm payrolls rose 172k in May, far above consensus of 85k and the 92k whisper. There were also large upward two-month revisions totaling +93k jobs, while the unemployment rate remained stable at 4.3% unrounded. The market responded by pricing close to one Fed hike through year-end, and the 10-year yield moved back through 4.5%. The bottom line is that strong job growth plus stable unemployment increases the risk of a longer Fed pause. Actual rate hikes are still viewed as unlikely, but the report clearly reduced the market’s comfort with the soft-landing / eventual-easing narrative.

The equity reaction was highly factor-specific. The hardest-hit pockets were exactly the most extended and speculative parts of the market: 12-month winners, drones, space, quantum computing, Bitcoin sensitives, and non-profitable Tech, all down more than 10%. This was a classic high-momentum de-risking event. Importantly, S&P ex-AI finished unchanged on the day, which is the key tell. The market was not broadly collapsing; it was aggressively repricing the most crowded AI, speculative growth, and high-duration winners.

This distinction matters because the weekly flow picture was more benign than the headline price action implied. At the client level, overall flow skews were benign, with a clear broadening dynamic under the hood. Megacap supply was a persistent trend over the last several sessions, likely used to fund other trades, including the GOOGL offering and expected future issuance. Against that, there was demand in Health Care, especially MedTech, Pharma, and Managed Care, as well as Financials. In other words, investors were not simply selling equities; they were rotating out of crowded winners and into laggards and under-owned defensives/cyclicals.

Prime brokerage data reinforces that point. Hedge funds net bought US equities for a third straight week and at the fastest pace in more than six months, driven by long buys outpacing short sales across both single stocks and macro products. Eight of eleven sectors were net bought, led by Industrials, which saw the largest net buying in nearly five months. Info Tech, however, has seen de-grossing in five of the last seven weeks, indicating that even before Friday’s selloff, funds had been reducing exposure in the most crowded Tech complex.

Leverage also moved lower. US long/short gross leverage fell 2.1 points to 208.4%, which is only the 8th percentile on a one-year basis. Net leverage fell 1.3 points to 53.9%, still the 66th percentile on a one-year basis. This is a nuanced setup: gross is very low, suggesting funds are not running highly expanded books, but net remains above median, meaning directional exposure is still meaningful. That can create vulnerability to beta shocks, but the low gross reduces the risk of a classic high-leverage unwind.

TMT: AI Resilience Tested, but Vol Did Not Confirm Panic

TMT was the epicenter of the selloff. The combination of AVGO’s post-earnings weakness, Anthropic recursive learning headlines, higher rates, and growing focus on equity supply/issuance challenged the resilience of the AI/Semis trade. The market had entered the week with extremely elevated expectations for AI infrastructure, and AVGO’s result was not enough versus a very high bar. That mattered because Broadcom has been a key symbol of custom silicon, networking, and AI infrastructure enthusiasm.

The Anthropic recursive learning headlines added a second narrative shock. The market has become increasingly sensitive to any AI development that could either accelerate disruption, compress software moats, or shift perceived winners and losers within the AI ecosystem. In a crowded tape, even ambiguous headlines can trigger selling if investors are already looking for a reason to reduce exposure.

Despite the magnitude of the price moves, the volatility response was unusual. SPX, NDX, and even SOX vol were down across the curve on the day, and derivatives desks saw very little panic hedging demand. That suggests investors were not rushing to buy protection after the fact. Instead, the move looked like a fast factor unwind in an already overextended group, with long holders reducing exposure and systematic or momentum-sensitive flows exacerbating the downside.

Next week’s TMT focus turns to WWDC, ORCL earnings, and several software investor days and user conferences, including NET, RBRK, and DDOG. The desk will be watching for positive AI datapoints that can stabilize the narrative. The key question is whether AI-related news can re-anchor the trade after the AVGO and Anthropic-driven reset, or whether investors continue to rotate out of the most crowded AI winners into broader market laggards.

Consumer: Heavy Tape, but Less Bad Than the Index

Consumer traded heavy early in the week and remains inversely correlated with momentum. Because Consumer has often acted as a relative beneficiary when Tech/Momentum sells off, Friday’s decline in the group was less severe than the broader market. The standout areas were gaming, lodging, and leisure, with the GS Gaming basket up 4% on more M&A headlines and better fundamentals relative to retail.

Retail remains more challenged. More companies confirmed a slowdown to start 2Q, including ULTA and LULU. These are partly idiosyncratic, but investor psychology is shifting. Investors are focusing more on the companies that are admitting trends have slowed, rather than rewarding those saying trends remain resilient. This creates a tougher setup for discretionary stocks with high expectations or weakening traffic, especially if higher oil and higher rates begin to weigh on the consumer.

Financials: Clean Rotation Beneficiary

Financials outperformed the S&P by roughly 400bps on the week, reinforcing the sector’s role as one of the cleanest inverse plays to Tech and Momentum. Upside was led by banks, especially money centers, followed by trusts and regionals. Large banks remain investors’ favorite way to play a bullish capital-markets backdrop, particularly if equity issuance, IPO activity, and trading volumes remain robust.

Traditional asset managers also performed well and, alongside banks, are now viewed as among the top “clean” longs left in Financials. Wealth and retail brokers saw a quiet relief rally as investor attention around terminal growth risk shifted toward exchanges. Exchanges traded down 5% to 17% last week, with CBOE and MIAX at the high end of the downside, as investors digested potential threats to retail trading volumes from regulated perpetual futures following Coinbase and Kalshi announcements.

Real estate feedback from NAREIT was constructive. Investor feedback was notably positive on Lodging, which outperformed REITs by about 800bps, and Residential, which outperformed by about 400bps. Next week brings a major mid-quarter Financials conference. Investor inbounds on banks largely expect neutral to positive updates, though there is some vigilance around signs of more intense deposit competition.

Energy: Bullish Bias Despite Volatile Oil Headlines

Energy gained about 2% over the last five days, though it remains down 3% over the last month. Investors broadly remain bullish on the setup for Energy equities and are looking to buy dips tied to potential Middle East resolution headlines. The logic is that even if oil gives back some geopolitical premium, the underlying setup for Energy equities remains attractive enough for investors to add exposure on weakness.

OFS sentiment remains broadly strong across North America and international markets, despite softer price action in OIH. Refining has also seen more recent bullish sentiment. In natural gas, US Henry Hub feedback remains more bearish, while specialists highlight relative bull cases for TTF into the summer and fall. The most asked-about names include XOM, PSX, VG, LBRT, DVN, and SU.

Weekend OPEC headlines will be important for next week. With oil still a key input into the inflation and consumer debate, any additional crude strength could amplify the post-NFP rates concern and keep pressure on long-duration equities.

Industrials and Materials: Relative Strength, but Speculative Areas Hit

Industrials rose about 100bps last week, while Materials fell 60bps, both outperforming the broader market, which was dragged lower by Tech. Upside in Industrials was led by several idiosyncratic winners. TMHC rallied after agreeing to be acquired by Berkshire Hathaway at a 24% premium. SAIC rose 10% after earnings came in well ahead of expectations and the company raised full-year EBITDA and EPS guidance early in the fiscal year. ODFL rose 8% after monthly tonnage and pricing data came in ahead of expectations. JCI also rose 8% after raising organic growth guidance around its Gemba investor day.

The weaker areas were the more speculative industrial growth names, including RKLB, FLY, KRMN, and AVAV, down 10% to 20%. This matches the broader market pattern: speculative, high-duration, high-multiple winners were hit hardest, even outside traditional Tech. F reversed recent strength and fell 15%, while HON dropped 9% after its aerospace investor day underwhelmed, with in-line top-line growth and a muted 9% EBIT CAGR that could be lumpy through 2030. Airlines were also weak, including AAL, UAL, and ALK, as crude reversed higher during the week.

Next week brings another large Industrials and Materials conference in Chicago, plus earnings from LEN and CNM, along with quarter-end checks.

Next Week: CPI, Fed Blackout, ECB, IPOs, Conferences, and OPEC

The S&P implied move through next Friday is 1.66%, which is meaningful but not extreme given the number of catalysts. The main macro focus is CPI on Wednesday, especially after the hot payrolls print. A sticky CPI print would reinforce the “longer Fed pause” narrative and could keep pressure on high-duration Tech and momentum. A softer CPI print would help markets look through the payroll strength and could support a bounce in risk assets.

The Fed enters its blackout period ahead of the June 17 rate decision, which reduces the ability of policymakers to shape expectations in real time. That means the market will be more dependent on the data itself and on rates-market interpretation. The ECB rate decision on Thursday adds another macro layer, especially for FX and global rates.

On the micro side, the IPO calendar remains busy, sell-side conferences are active, and the GS Healthcare Conference runs Monday through Wednesday. Given recent demand for Health Care, especially MedTech, Pharma, and Managed Care, that conference could matter for continued broadening. Weekend OPEC headlines also need to be watched because crude remains central to the inflation and consumer narrative.

Friday was a major risk-off event at the index level, but the underlying message was more nuanced. The selloff was concentrated in the most crowded and extended parts of the market: AI, Semis, momentum, speculative Tech, crypto-sensitive equities, drones, space, quantum, and 12-month winners. S&P ex-AI was unchanged, which shows that the broader market did not collapse. Instead, the market continued to broaden beneath the surface, with flows favoring Health Care, Financials, Industrials, and other laggard or under-owned areas.

The hot NFP print changed the macro debate by increasing the risk of a longer Fed pause, while the market briefly priced close to one hike through year-end. That is a problem for high-multiple, long-duration, crowded Tech, especially after AVGO failed to clear the bar and the AI narrative was hit by Anthropic headlines. However, the lack of panic hedging and the decline in vol across the curve suggest the move was more of a positioning and factor reset than a systemic de-risking.

The key question for next week is whether CPI confirms or offsets the NFP shock. If CPI is benign, the market can likely stabilize and the broadening trade can continue. If CPI is hot, the combination of higher rates, oil uncertainty, IPO supply, and stretched AI positioning could produce another leg of factor volatility. In that environment, the cleanest stance remains selective: be cautious on crowded AI/momentum and speculative winners, but look for opportunities in Financials, Health Care, Industrials, select Consumer services, and other areas benefiting from broadening.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!