FTSE Finish Line: June 11 — Hormuz Headlines, but Banks and Miners Drive the Bounce

FTSE Finish Line: June 11 — Hormuz Headlines, but Banks and Miners Drive the Bounce

London pushed firmly higher on Thursday, shrugging off another escalation in the Middle East as banks, insurers and miners dragged the FTSE 100 back onto the front foot. The benchmark was up over 1.3%, even as Iran announced the closure of the Strait of Hormuz following a fresh round of U.S. military strikes on Iranian targets. On paper, the geopolitical backdrop should have been a clear risk-off catalyst. Tehran warned of retaliation and said the already fragile ceasefire in the three-month conflict had become “practically meaningless". The Strait of Hormuz is one of the world’s most important oil transit routes, so the announcement immediately raised the risk of energy disruption, another inflation shock and renewed pressure on global central banks. But the equity tape told a more nuanced story. Investors did not abandon UK risk; they rotated into the parts of the market that benefit from higher yields, stronger commodity pricing and global exposure. Financials led from the front. HSBC and Standard Chartered both gained 2.8%, reversing recent weakness in Asia-exposed banks. NatWest rose 1.5%, while Barclays and Lloyds added 1.2% and 1.1%, respectively. The move suggested that the market was willing to buy banks again as long-end yields remained elevated and geopolitical risk kept rate-cut expectations contained.

Miners also helped carry the index. Anglo American, Rio Tinto and Fresnillo rose between 1.2% and 2%, while Glencore and Antofagasta posted more moderate gains. The sector’s strength pointed to a shift away from Wednesday’s growth-scare selling and toward a renewed commodity hedge as Middle East tensions intensified. Fresnillo’s gain also reflected interest in precious-metal exposure as geopolitical risk stayed high. Insurers and broader financials joined the rally. Prudential climbed nearly 4%, one of the strongest FTSE 100 performers, while Aviva and Standard Life also advanced. 3i Group gained, and Intertek rose 2.7%. Among consumer and cyclical names, Kingfisher, Burberry and Next advanced between 2% and 2.5%, while JD Sports, Airtel Africa, Rolls-Royce, BAE Systems, SSE and Centrica also traded notably higher. Defence exposure remained supported, with BAE Systems rising as investors continued to price a world of higher geopolitical risk and increased defence spending. Energy-linked Centrica and utility names also found demand, reflecting the market’s preference for cash-flow resilience and exposure to structurally supported themes.

The session’s major casualty was Halma. Shares in the health and safety technology group plunged 14% after the company issued disappointing guidance for the year ahead. The scale of the move showed that investors remain unforgiving toward premium-rated quality names when forward expectations are reset lower. In a market still wrestling with elevated yields and macro uncertainty, valuation discipline remains harsh. Other laggards included ICG, down more than 3%, and Sage, off 2%. Spirax, Barratt Redrow, Berkeley Group, Endeavour Mining and Auto Trader fell between 0.7% and 1.25%. The weakness in housebuilders contrasted with the broader market gain, suggesting that domestic rate-sensitive exposure remains vulnerable even on stronger index days.

Property data came in tepid. The Royal Institution of Chartered Surveyors reported that the UK house price balance was unchanged at -35% in May. That remains a weak reading, but some underlying measures suggested tentative stabilisation in the property market. For housing equities, however, stabilisation is not the same as recovery. Affordability pressure, high mortgage rates and uncertainty around the Bank of England’s path continue to cap enthusiasm. The bigger macro tension is that Middle East escalation is once again pushing markets toward a familiar contradiction. Higher energy risk can support commodity stocks, banks and defence, but it also threatens inflation, consumer confidence and rate-sensitive domestic sectors. Thursday’s market chose to focus on the winners: financials, miners and global cyclicals. But the risks underneath did not disappear.

Finish Line: The FTSE 100 rallied over 1.3% even as Iran announced the closure of the Strait of Hormuz, with banks, miners, insurers and selected cyclicals overpowering geopolitical caution. HSBC, Standard Chartered, Prudential and the miners gave the index its lift, while Halma’s 14% plunge was the clearest reminder that guidance risk is still being punished hard. The tape is not ignoring Middle East escalation — it is repricing around it. For now, that means buying banks, commodities and defence, while staying wary of expensive quality and rate-sensitive domestic names.

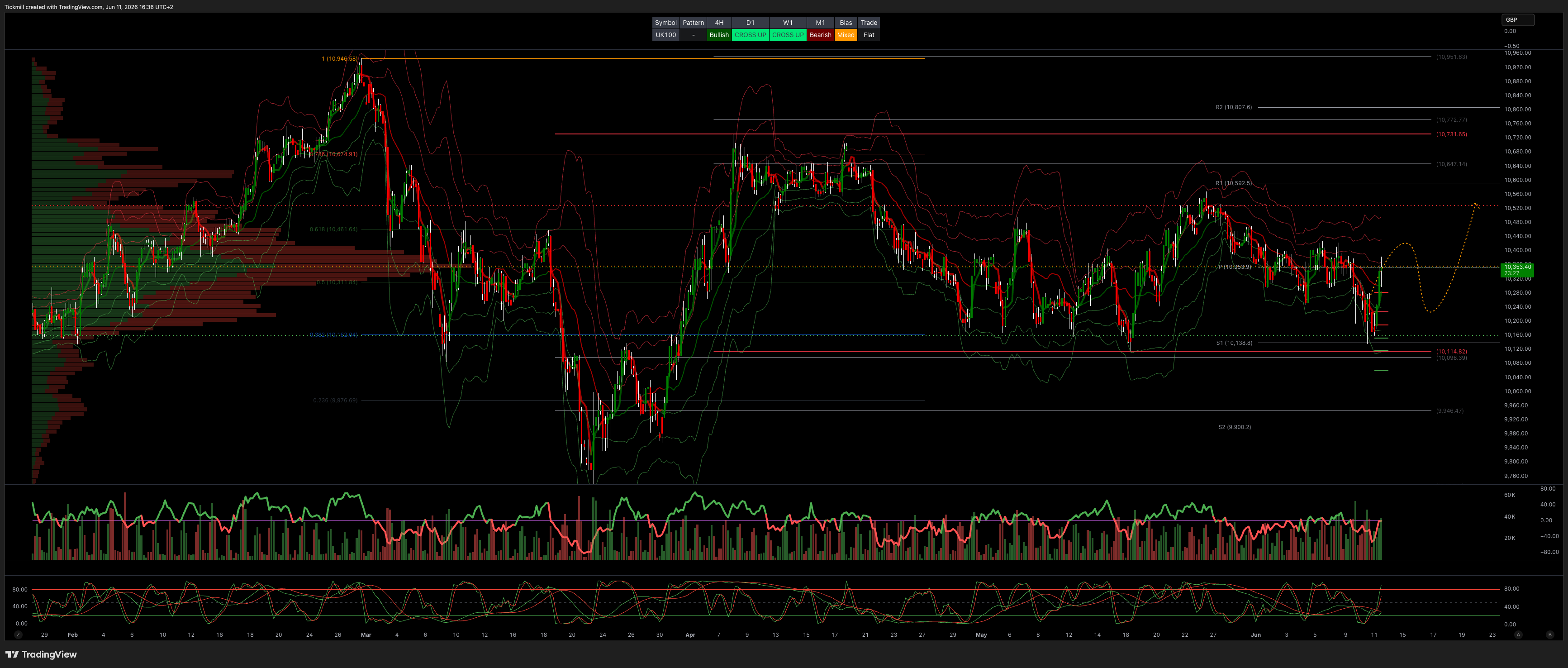

TECHNICAL & TRADE VIEW – FTSE100

Daily VWAP Bullish

Weekly VWAP Bullish

Above 10500 Target 11000

Below 10100 Target 9469

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 71% and 74% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!